AT A GLANCE:

- An already growing national preference for protein is supported by new dietary guidelines and GLP-1s.

- U.S. beef and veal consumption now exceeds domestic production, driving increased imports.

A shift in national food and nutrition is underway, fueled in part by the recently redesigned food pyramid released by the U.S. Departments of Agriculture (USDA) and Health and Human Services (HHS), coupled with a rising percentage of the population now taking GLP-1 medication. These factors put demand front and center, marking a change from recent decades where agricultural markets were dominated by supply-side forces.

A Dietary Shift as GLP-1s Sweep the Nation

The Food Movement stalwart Michael Pollan summarized his dietary philosophy in his 2008 book In Defense of Food as follows: “eat food, not too much, mostly plants.” Now 18 years later, Pollan skeptically summarizes the latest nutritional guidelines from the USDA and HHS with an ironic spin on his mantra: “eat food, (probably) not too much, mostly meat.” Many of the USDA and HHS recommendations bear similarity to those of the old Food Movement of Pollan and coastal chefs, like Alice Waters and Mollie Katzen, including portion control and prioritizing whole, minimally processed foods. However, the new pyramid promotes animal protein—in particular via bovine products like beef, dairy and even tallow—like never before. While the new nutritional guidelines outline the importance of eating fresh, whole fruits and vegetables each day, that recommendation comes below an emphasis on animal protein.

Today’s new guidelines have emerged in conjunction with another massive force in the national dietary landscape: the increasing use of GLP-1 medications. According to Gallup polling, over 12% of Americans have taken GLP-1 medication, a class of drugs known to effectively assist in weight loss through increased satiety and, thus, less caloric consumption as of late 2025. People taking GLP-1 medications report shifting their dietary priorities away from sugar and starches toward more nutritionally dense, higher protein foods. Researchers postulate that this change in preference comes from the body’s natural coping mechanism for consuming fewer calories: When you’re not eating as much, you need to make each calorie count.

Given the enormity of the American food system, dietary trends do not always make a meaningful show in national data. The shifting American preference toward protein, however, has proven fundamental enough to influence national supply statistics. Demand is now a central focus in U.S. agricultural markets: a marked change from the previously prevailing narrative where U.S. agricultural markets focused almost exclusively on supply, and demand moved either extremely slowly or primarily in response to supply. Additionally, making a mark in national health data, the increased use of GLP-1 drugs is widely understood to be the conduit for declining obesity. The average American obesity rate has declined to 37% of U.S. adults, from just below 40% three years ago, according to the Gallup National Health and Well-Being Index.

American Taste for Beef Persists, Despite Headwinds

Beef is expensive, and yet against this and other significant headwinds, domestic demand for beef is only rising. To put the increased cost of beef into perspective: the percentage change in beef prices from the year 2000 to present is approximately equal in magnitude (3.5 times) to the increase from the year 2000 to the peak of the avian-flu-induced spike in egg prices in early 2025, according to the Bureau of Labor Statistics. Contradicting new USDA and HHS recommendations, beef faces some headwinds in terms of health perception, as some research suggests negative effects of excessive red meat consumption on longevity. Beef, additionally, is more resource intensive in its production than other sources of protein in terms of water, land and feed use and is thus associated with significantly greater greenhouse gas emissions compared to other sources of protein.

Regarding the current state of high beef prices, “we are in a classic cattle cycle,” observed USDA Chief Economist Justin Benavidez at this year’s USDA Agricultural Outlook Forum. Dating back to the late 19th century, the cattle cycle is a theory that seeks to explain the ebbs and flows of U.S. cattle inventory. Each of the last observed cycles have spanned 10-14 years, and now in year 12 of the current cycle, the U.S. cattle industry has long been locked in the contraction phase, characterized by high cattle and carcass prices and low herd numbers.

The industry is waiting with bated breath for herd expansion (initiated by what is known as “heifer retention”) and a new cattle cycle to begin, potentially softening prices. Climatic factors this year, however, may be an impediment to a new cycle. Dryness out West is looking likely, including in the Northern Panhandle, making this upcoming fire season a risk cattle producers are closely monitoring.

While cattle head has been declining for years, down nearly 35% in 2026 since its peak in 1975, advances in genetics and feed have allowed producers to yield more meat per animal in less time. As a result, total beef production in the U.S. has not followed headcount downward, though in recent years, total domestic consumption of beef and veal has exceeded domestic production to a degree not seen since the mid-2000s, spurring increased imports.

With a variety of uncertainties within the cattle market, more market participants are turning to the futures market to manage risk. Live Cattle and Feeder Cattle futures prices have been mounting since mid-2020, with record highs for Feeder Cattle in October of 2025. Reflecting the life cycle of the underlying herds, Live Cattle futures then peaked months later, in February of 2026.

A Growing Meat Pie

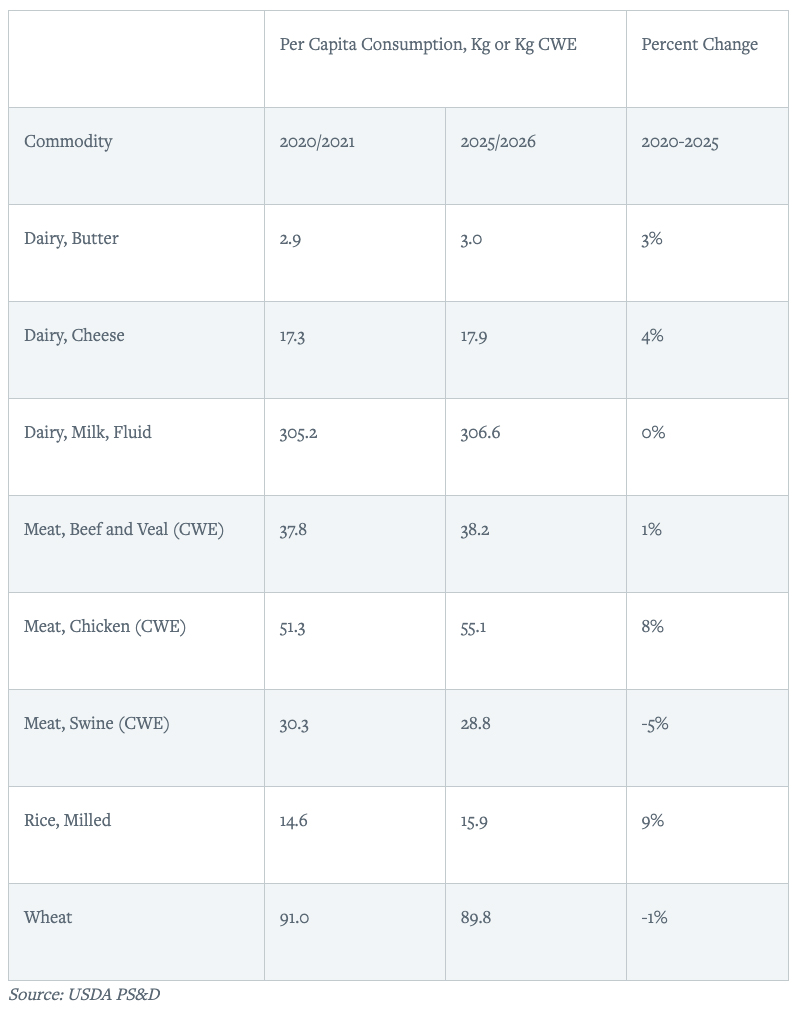

In economics, when one good becomes more expensive, it is assumed that it will be substituted with a functionally equivalent, but less preferable good. In this case, when beef becomes more expensive, the expectation may be substitution with poultry or pork. In the instance of meat protein, however, the pie has only grown. The current preference for protein seems to be a continuation of dietary shifts observed over recent decades. Since the marketing year 2020, total national consumption of beef and veal has increased 5.3% to the current year, despite decreased herd numbers. Total pork and chicken consumption combined increased by more than 7%, marking per capita growth across combined meat species.

Per Capita Consumption of Animal Proteins Increase

At the same time, some carb-based metrics, such as wheat milling, have declined. U.S. domestic wheat consumption per capita is down 1% since 2020 and 30% since the year 2000, with a small share of that consumption replaced with rice, which increased by 21% per capita over that period. This data reflects the broader shift to a more animal-protein heavy diet over the 21st century.

Notably, corn and soybean markets in the U.S. are primarily influenced by factors other than direct food demand since relatively little of those crops are directly consumed by people. Corn and soybeans, rather, typically serve primarily as inputs to animal feed and feedstocks for biofuels to be blended domestically and for export abroad.

An Unequal Recovery

A diet increasingly oriented toward animal protein doesn’t come cheaply. While the U.S. population as a whole may be seeing a shift toward higher protein diets, not all Americans are well-positioned to spend an increasing amount on food.

Economists have noted a K-shaped recovery from 21st century recessions, where the relatively affluent portion of the population sees increasing prosperity while a large subset of the population continues to struggle economically. While an increasing percentage of Americans have taken GLP-1 drugs, those drugs are currently very expensive, even when health insurance has been applied, making them accessible primarily to the population signified by the upward prong of the K curve. Accordingly, the USDA recently observed that while national obesity has declined, obesity has actually increased among rural populations, noting that rural Americans tend to experience more poverty than urban Americans.

Looking Ahead

As the U.S. agricultural and dietary landscape moves further into 2026, the traditional supply-side dominance of agricultural markets will likely continue to meet powerful, demand-driven forces. The convergence of new federal nutritional priorities and the pharmaceutical revolution of GLP-1s has supported an already growing national preference for protein over starch, even in the face of high prices and environmental headwinds. While new national dietary guidelines may be in focus at the moment, the data paints a picture of a national diet and agricultural landscape changing with the times.

CME Group futures are not suitable for all investors and involve the risk of loss. Full disclaimer. Copyright © 2026 CME Group Inc.