The investing world is awash in economic data. Amid this potential data overload, how does an investor separate truly useful data from the noise? For example, quarterly gross domestic product (GDP) reports provide a decent snapshot of economic activity over the previous three months but won’t provide any useful information about where the economy is heading. Unfortunately, as a lagging economic indicator, GDP can only tell you what has happened—not what will happen.

Fisher Investments believes leading indicators are more useful in helping investors gauge the path forward. These indicators are especially important when making economic forecasts, which are critical to determining the outlook for stocks. But, how do you find the right leading indicators? It would be time consuming to sort through all possible options, and one indicator alone doesn’t tell you much. Fortunately, you can use a combination of several leading indicators that have been remarkably effective at forecasting economic direction. The Leading Economic Index (LEI) combines an assortment of such indicators, and this article will discuss how you can use it to evaluate the economy.

A brief history of the LEI

Economic statistics gained popularity in the wake of the Great Depression. Around this time, the National Bureau of Economic Research (NBER) collected a variety of data points that seemed to lead the economy or move ahead of the rest of the pack. These data points were eventually combined to form the LEI.

Manufacturing dominated the US economy at the LEI’s inception, which is why the index’s factors initially centered on this industry. The first iteration of the LEI included data such as the Dow Jones Industrial Average (DJIA); durable goods orders; residential, commercial and industrial building contracts; and the average manufacturing workweek. While most of these indicators were informative for the US’s post-war, manufacturing economy, seismic economic shifts since then have prompted changes to the LEI.

The LEI, today

Control of the LEI eventually passed to The Conference Board, a US-based research nonprofit, in the mid-1990s. The structure of today’s LEI reflects the lessons learned over time. The broader, capitalization-weighted S&P 500 replaced the narrowly focused, price weighted DJIA to better represent the US stock market. Some factors, like commodity prices and business incorporations, lost their place entirely. Other factors, such as the important interest rate spread (10-year Treasury minus federal funds rate) didn’t appear until the late 1990s. Exhibit 1 shows the 10 current components of the US LEI.

Besides the US LEI, The Conference Board also administers LEIs for 11 other major countries and the eurozone. LEI inputs can vary slightly by country.

Predictive “power”

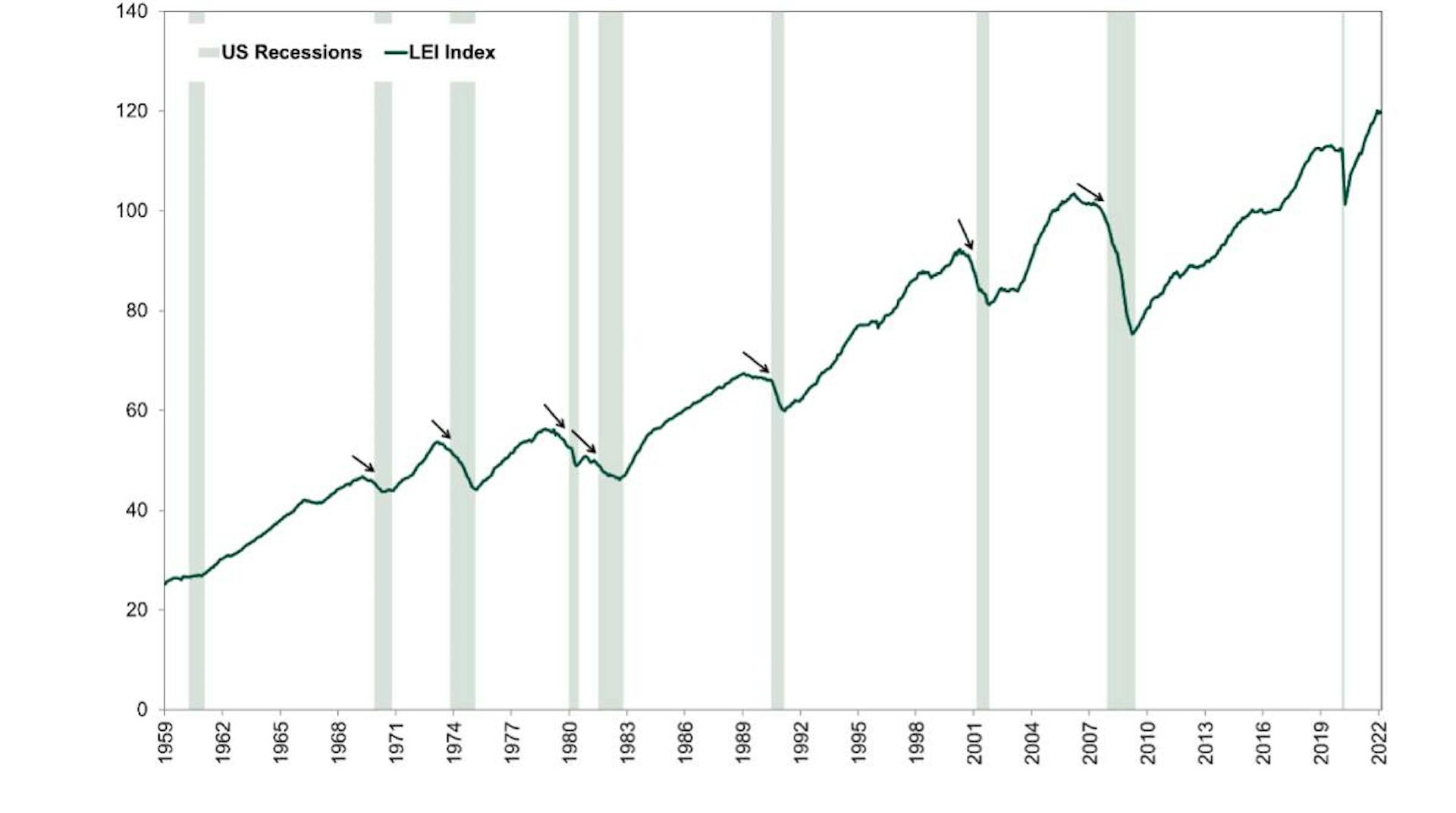

Because its components focus on future economic activity, the LEI tends to be a reasonably accurate (though, not perfect) recession predictor. As Exhibit 2 shows, over the last 60 years, a sustained decline in the LEI has preceded all but two US recessions. Notably, the 2020 recession was one of those instances. However, 2020’s steep economic downturn didn’t resemble a traditional recession. Government-mandated business closures in an effort to contain COVID-19 drove 2020’s abrupt economic contraction—an unprecedented scenario well outside the LEI’s scope.

Exhibit 2: US LEI and Restrictions

The limits of the LEI

Like any economic indicator, the LEI can send false signals. For example, the US LEI has occasionally dipped for several months before reaccelerating without an ensuing recession. In October 2019, for example, the US LEI’s six-month trend turned negative. Fisher Investments didn’t believe this change necessarily pointed toward a looming recession. Instead, ongoing troubles in US manufacturing—notably in the shale oil and automotive industries—had a disproportionate drag on the LEI that skewed results. This highlights the importance of examining what factors are influencing the LEI before declaring a recession is imminent.

Similarly, the LEI isn’t a great timing tool for stocks—partially because stock prices are one of its components. Stock markets pre-price all widely known information and often fall in advance of a recession. LEI’s have trended negatively for varying periods of time before recessions occur. However, it is important for stock forecasters to be aware of how all the LEI’s components work to help gauge the probability of future recessions.

The LEI has been an effective tool for stock market forecasters. Every indicator has its shortfalls, but few have been as reliable as the LEI. So, check LEIs from around the world when fears spread about an economic slowdown or recession. Are they rising, falling or holding steady? If they are falling, examine the reasons closely so you can build an informed opinion of whether recession fears are valid or just noise. Consulting the LEI can help you make better investment decisions so you can stay on track to reaching your long-term financial goals.

Investing in stock markets involves the risk of loss and there is no guarantee that all or any capital invested will be repaid. Past performance is no guarantee of future returns. International currency fluctuations may result in a higher or lower investment return. This document constitutes the general views of Fisher Investments and should not be regarded as personalized investment or tax advice or as a representation of its performance or that of its clients. No assurances are made that Fisher Investments will continue to hold these views, which may change at any time based on new information, analysis or reconsideration. In addition, no assurances are made regarding the accuracy of any forecast made herein. Not all past forecasts have been, nor future forecasts will be, as accurate as any contained herein.